How Atal Beemit Vyakti Kalyan Yojana is Beneficial for Employees?

How Atal Beemit Vyakti Kalyan Yojana is Beneficial for Employees?

The central government launched a scheme “Atal Beemit Vyakti Kalyan Yojana”. It was introduced on 1-07-2018. This scheme provides welfare measures for the employees who lost their job during a pandemic. Section 2(9) of the ESI act 1948 is covered under it. This act is in the relief payment form given for up to 90 days once in a lifetime.

ABVKY was launched for two years on a pilot basis. Till June 2022 the scheme has been extended now.

Benefits under the scheme

Under the extended ABVKY scheme the rate of relief has been improved.

- The eligibility conditions for insured persons have been relaxed who became unemployed from pandemic time.

- The relief rate of the employee has been doubled from 25-50% average earning per day.

- The insured person can make a direct claim to the ESIC Branch without involving the last employer.

- After the date of unemployment, the claim may become due for 30 days. Before this, the time was for 90 days.

- There is no need to forward the claim of the insured person by the employer. The claim can be submitted completely online in the prescribed claim form. It can be submitted directly to the branch office also.

Eligibility

- The factories, industries, and private companies, employees can take the ABVKY benefits.

- The employee can claim the benefit with the use of documents provided by the company or with an ESI card.

- The salary of those people, which is less than RS.21000, can get the benefits of ABVKY.

- In the case of especially disabled people, those with a salary is less than RS 25000 can take benefits of ABVKY.

- For a minimum of two years of the time period, the insurable employment should be taken by the insured person. It should be before his/her employment time period.

- For immediate preceding unemployment the insured person must have contributed to ESI. in the contribution period, it should not be shorter than 78 days

- As per the notification from the government, the contribution must have been payable or paid by the employer.

- The benefits cannot be given to the person who has lost his job. It can be due to misconduct, punishment for voluntary retirement, or superannuation.

- The aadhaar card and account in the bank of the insured person must be merged with the database.

- The workers can only file the claims to take the scheme benefits.

Termination or Disqualification of relief under ABVKY

Under ABVKY the relief cannot be allowed in the consecutive circumstances:

- Contributory service for less than two years,

- On the death of an insured person,

- On attaining the pension age,

- Making use of strikes by the employees and illegally declared by the competent officer,

- In case of premature retirement or spontaneous retirement,

- Voluntary forsaking of the employment,

- Punishment under the provision of ESI ACT in section 84,

- On being re-employed and is still under the ABVKY receipt of relief,

- Termination of the employee under disciplinary action,

- During lockout or lockdown.

Calculation of the relief amount

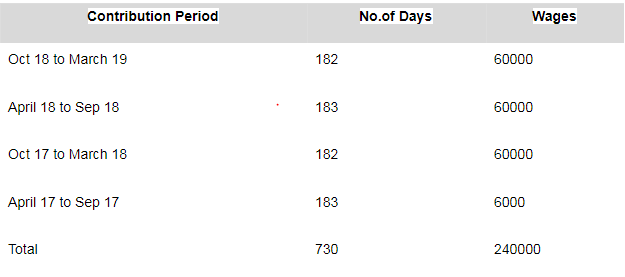

Illustration-1

Date of Unemployment: 01/04/2019

Contributory particulars of the preceding four contribution periods:

The amount of benefit/relief available for 90 days: (2,40,000/730) x (25/100) x 90 = Rs.7397/-

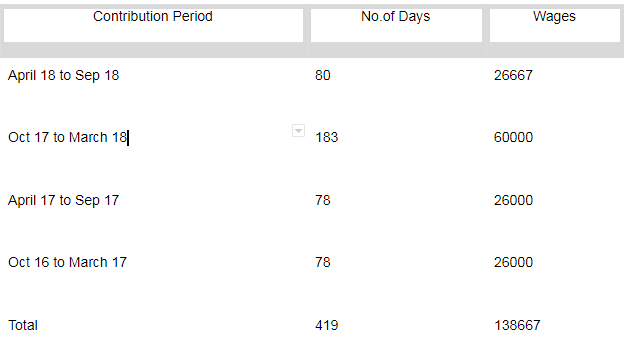

Illustration-2

Date of Unemployment: 02/10/2018

Contributory particulars of the preceding four contribution periods:

Amount of Benefit/relief available for 90 days:- (1,38,667/730) x (25/100) x 90 =Rs.4274/-

For relief submission of claim

- Under this scheme, the claim for the relief can be submitted anytime by the claimant. But he should be rendered as employed. It can be submitted to the appropriate branch office in the form of an affidavit in the prescribed form.

- The submission cannot be done later than one year from the date of unemployment.

There will be no allowance for the claim of relief under ABVKY for any future period. - The submission of the claim by an insured person will be to his designated branch office.

- To generate a claim for ABVKY, a link will be given in the ESIC portal. The insured person will put all the required details and the link will be opened.

- The system will check whether the IP is eligible for relief. If yes, then it will send the AB-1 form of claim and AB-2 form of forwarding letter from his last employer. It will also include instructions for the IP.

- If in case the person is not eligible then a regret message will be sent to IP.

- The eligible IP will take the printout of the claim submitted and a letter to the employer. Then the duly signed claim in the affidavit and the forwarding of the employer will be submitted. It is done to his designated branch office.

- Generation of every claim will have an auto-generated unique ID Number.

- On the claim receipt, the details given by the IP Applicant will be checked by the staff system. It will be done under the supervision of the Branch Manager at the Branch Office. Thus the system will calculate the eligibility for relief under the scheme.

- The claim will be set on the quantity to which the claimant is entitled. It is based on IP’s details, contribution, as well as details available on the system.

- The relief payment will be done to IP’s bank account.

Payment Mode

- Under this scheme, the relief will be paid or payable by a branch office. It will be to IPs bank account directly & electronically.

- In case of IP’s death, the amount will be paid to his/her legal heir/ nominee by the account payee cheque only.

- The bank account details of the claimant is a precondition for claiming relief mentioned in the ESIC database. If in case the claimant bank account details are not available. Then the brank manager will authenticate on the basis of the canceled cheque leaf. He can also check it with the bank account having the name of the claimant on it. The information will be provided by the claimant along with a claim for this relief.